Guam Public School System

FY 2005 Financial Highlights

June 29, 2006

The Guam Public School System (GPSS) continues in its third year on high-risk status, since September 2003, for failing to submit financial audits for five years (FY 1998 through FY 2002). However, for the first time since the designation by the U.S. Department of Education (USDOE), independent auditors, Deloitte & Touche expressed an unqualified opinion on the GPSS FY 2005 financial statements. In prior years, audit qualifications resulted from inadequate internal controls, and inadequate documentation of fixed assets and non-appropriated funds.

According to USDOE officials, the high-risk status will remain until GPSS can prove accountability through consistent unqualified audits and improvements to its programmatic and fiscal systems. The unqualified opinion is a step in the right direction to ultimate removal of GPSS’ high-risk status.

To improve the accounting infrastructure, GPSS hired a Chief Financial Officer in February 2006, after a seven-month vacancy of the Comptroller position. Despite the improvements, the financial condition of GPSS has deteriorated to a $42.1 million deficit and questioned costs of the expenditure of federal funds have increased by $1.1 million to $1.5 million in FY 2005 from $365,000 in FY 2004.

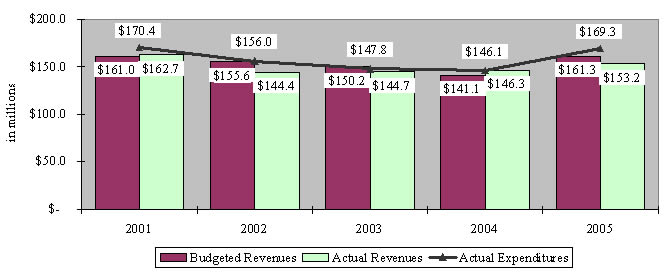

Financial Statements The GPSS general fund reported over-expenditures of $16.1 million compared to an under-expenditure of $160,000 in FY 2004. Except in FY 2004, GPSS has consistently over-expended both budgeted and actual appropriations as the chart below demonstrates.

The current $16.1 million over-expenditure has caused the GPSS general fund deficit to climb to $42.1 million from $25.9 million in FY 2004. This was mainly due to GPSS receiving only $153.2 million, or $8.1 million less than the anticipated $161.3 million in appropriations but also spending $8 million over budgeted amounts. GPSS also incurred a $3.8 million liability for teachers’ salaries following an April 2006 court order. Utilities, in particular, have been under-funded as illustrated in the table below.

Utilities Funding

|

Budget |

Actual |

Variance |

2001 |

$ 4.0 million |

$ 11.6 million |

$ (7.5) million |

2002 |

$ 5.6 million |

$ 10.9 million |

$ (5.3) million |

2003 |

$ 4.5 million |

$ 6.9 million |

$ (2.3) million |

2004 |

$ 6.0 million |

$ 11.2 million |

$ (5.2) million |

2005 |

$ 8.0 million |

$ 11.1 million |

$ (3.1) million |

Because of the funding deficiency, cash balances have declined by $11.2 million to $1.1 million from $12.3 million in FY 2004. In FY 2005, GPSS received $52.2 million in federal grants and contributions, $4.2 million more than the $48 million received in FY 2004.

Prior years’ obligations include the Retirement Fund and the Guam Power Authority (GPA). GPSS owes the Retirement Fund $16.7 million (includes $3.5 million interest and penalties) for FY 2003 contributions. During FY 2005, GPSS was current in its payments toward the $15.8 million GPA note and a $13.9 million balance remains. However, payments for FY 2006 are behind.

Single Audit ReportsIn FY 2005, the number of findings remained at 21, unchanged from FY 2004. However, questioned costs have soared to $1.5 million, or an increase of $1.1 million from $365,000 reported in FY 2004 and $765,000 more than FY 2003. Questioned costs exceeding $1 million were last reported in FY 2000.

Procurement findings resulted in 60%, or $889,000 in total federal questioned costs and an additional $511,000 was also questioned in local funds. For $793,000, emergency procurement was utilized for air conditioning and construction, however, competitive bidding should have been used because the solicitations were obtained outside the emergency period. For $472,000, potential bidders for construction, air conditioning, beverages, bread, and equipment were not given sufficient time to respond to bids.

Other questioned costs were the result of federal expenditures of $258,000 exceeding the period of availability, $214,000 expended without grantor approval, $92,000 deficient in local matching funds, and $17,000 expended beyond allowable administrative costs.

Problems in the accountability of GPSS’ non-appropriated funds continue and the auditors cautioned that funds might be used fraudulently. For example, supporting documentation was not maintained, payments were made for faculty and staff entertainment unrelated to the fund’s purpose, inconsistent monitoring, and referrals to the Attorney General’s Office for investigations. A recommendation was made to the Guam Education Policy Board (GEPB) to reconsider whether GPSS should continue to assume this costly responsibility. Alternatives include, outsourcing the service, fund collections disbursed through the central office, change in legislation, and handing the responsibility to other adjunct school organizations such as parent teacher organizations.

GPSS’ unresolved questioned costs (since FY 1998) are now $10.5 million.

Subsequent to September 30, 2005, the Superintendent of Education was terminated by the GEPB. In June 2006, a letter from the USDOE warned that commitments made by the former Superintendent were not reiterated by interim GPSS leadership and could adversely affect the availability of future federal grants.

See Management’s Discussion and Analysis for further details.